Geoff Hoffman

Chief Legal Officer •

Sydney

The Bill containing the legal framework for Australia's new internationally-aligned mandatory climate-related reporting regime, the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024, has been introduced into the House of Representatives.

It contains important modifications to the proposals made in the Exposure Draft legislation released earlier this year.

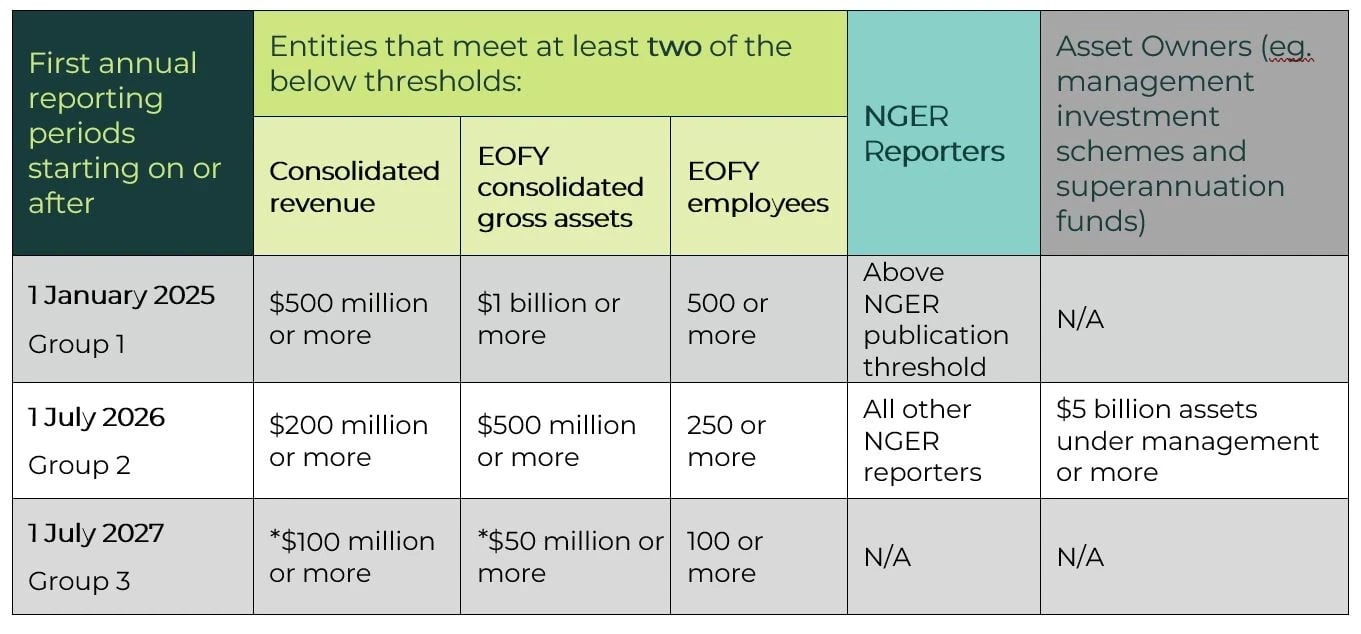

The Bill confirms that entities that are required to prepare and lodge annual financial reports under Chapter 2M of the Corporations Act will be required to also prepare a "sustainability report" in accordance with sustainability standards made by the Australian Accounting Standards Board (AASB), if they:

meet certain minimum size thresholds; or

have emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007 (Cth) (NGER Act); or

are asset managers (such as registered management investment schemes or registerable superannuation funds) and have a minimum value of assets under management.

The Bill retains the phased introduction of the reporting obligations. However, importantly, it is now proposed that Group 1 entities (below) will only be required to report from their first annual reporting period after 1 January 2025 (as opposed to from 1 July 2024 as was proposed in the Exposure Draft Legislation).

* thresholds increased per Federal Budget 2026-27 announcement https://budget.gov.au/content/factsheets/download/factsheet-regulatory-reform.pdf

* thresholds increased per Federal Budget 2026-27 announcement https://budget.gov.au/content/factsheets/download/factsheet-regulatory-reform.pdf

Entities which fall within Group 3 and have no material climate-related risks or opportunities will only be required to disclose a statement to that effect.

Entities that are not required to lodge financial reports under Chapter 2M of the Corporations Act are also exempt from preparing annual sustainability reports. This includes entities that are registered under the Australian Charities and Not-for-profits Commission Act 2012 (Cth), or entities that have been provided with relief or are exempt from financial reporting by way of an ASIC class order or individual entity relief.

Entities will need to prepare a sustainability report in addition to the existing directors report, financial report, and auditors report included in their annual financial report.

The sustainability report must include the entity's climate statements for the year which must comply with the sustainability standards which are being developed by the AASB. The AASB released Exposure Draft ED SR1 Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information, on 23 October 2023 for comment which closed on 1 March 2024. The Government intends that the sustainability standards will closely align with ISSB’s IFRS S2 Climate-related Disclosures Standards (IFRS S2).

The Minister may also, by legislative instrument, require a sustainability report to include other specified statements relating to financial matters concerning environmental sustainability.

In accordance with the Bill and the AASB sustainability standards, the climate statements will be required to disclose:

Risks and opportunities – for the entity, including information about material climate-related risks and opportunities for its business, as well as how the entity identifies, assesses and manages risk and opportunities.

Greenhouse gas emissions – any metrics and targets of the entity related to climate, including the entity's gross scope 1, 2 and 3 emissions (including financed emissions). The Bill proposes to align the definition of Scope 1, 2 and 3 greenhouse gas emissions with the definition given in the draft AASB sustainability standards. Disclosure of scope 3 emissions is only expected to be required from an entity's second reporting year onwards. Further, the Government expects that the Sustainability Reporting Standards adopted by the AASB will require disclosure of market-based (as opposed to location based) Scope 2 greenhouse gas emissions no later than 1 July 2027. The estimation methodologies and frameworks used should be consistent with those included in the National Greenhouse and Energy Reporting (Measurement) Determination 2008 where available, or the relevant annual National Greenhouse Accounts Factors publication, where entities are reporting Australian-based emissions.

Governance – information about the reporting entity's governance processes, controls and procedures used to monitor and manage climate-related financial risks, opportunities, metrics and targets.

Strategy – the entity's strategy for identifying and addressing climate-related risks and opportunities (including scenario analysis): including (i) a qualitative scenario analysis to inform the disclosures, moving to quantitative scenario analysis over time; and (ii) climate resilience assessments against at least two possible future states, one of which must be consistent with the global temperature goal set out in the Climate Change Act 2022 (Cth). The Government expects that the Sustainability Reporting Standards adopted by the AASB will permit entities to commence with qualitative scenario analysis for the purposes of their climate resilience assessments, with quantitative analysis required for financial years commencing on or after 1 July 2027.

Transition planning and climate-related targets – the entity's transition plans with offsets, target setting and mitigation strategies and any climate-related targets (if the reporting entity has them) and progress towards these targets.

Industry-based metrics – the entity would be required to have regard to disclosing industry-based metrics, where there are well-established and understood metrics available for the reporting entity (eg.area of properties located in 1 in 100-year flood zones, by property subsector). The Government expects that the Sustainability Reporting Standards adopted by the AASB will only require entities to disclose against industry-based metrics from 1 July 2030 onwards. Entities may choose to disclose relevant industry-based metrics voluntarily prior to that date.

The AASB (which is currently developing Australian climate disclosure standards) decided not to publish the industry-based guidance accompanying IFRS S2 or include references to Sustainability Accounting Standards Board (SASB) Standards, until the content has been comprehensively internationalised by the International Sustainability Standards Board (ISSB) and has undergone the AASB’s own due process.

The AASB is proposing to introduce an Australian-specific requirement that if an entity elects to make industry-based disclosures, the entity should consider the applicability of well-established and understood metrics associated with the business models, activities or other common features that characterise participation in the same industry.

Initially, the sustainability report will only be required to be reviewed or audited to the extent required by the audit standards made by the Australian Auditing and Assurance Board (AUASB).

Over time these standards are expected to evolve in terms of both the extent and level to which disclosures in the sustainability report will need to be assured. In March 2024, the AUASB released a consultation paper seeking high-level information feedback on the likely demand from users and directors for assurance over climate-related financial information in annual reports of entities in each of Groups 1, 2 and 3; the likely maturity of entity systems, process and information sources, including availability of any necessary assurance over information from value chains; and the likely ability of auditors and their experts to meet that demand.

The Bill provides that the sustainability report must be audited from 1 July 2030 and include an audit opinion (being a positive assurance the report complies with the Corporations Act and applicable AASB standards) from that time.

In the meantime, depending on the audit standards made by the AUASB, statements in an entity's sustainability report may be subject to no assurance – or only subject to a review and "review opinion" by its auditor. A "review opinion" is much lower standard of assurance than an audit – and only results in a negative assurance that in the course of its review the auditor has not become aware of any non-compliance.

As is the case with the financial report, the climate statements in the sustainability report will need to be accompanied by a directors' declaration stating whether, in the directors' opinion, the climate statements comply with the requirements of the Corporations Act and applicable AASB standards.

The ordinary form of the declaration (which currently applies to the financial report) is a positive statement that, in the directors' opinion, the report complies with the Corporations Act and applicable AASB standards.

Importantly, consistent with the delay in the commencement of audit and assurance processes, for the first three years the directors' declaration for the climate statements will only require a statement as to whether, in the directors' opinion, the entity has taken reasonable steps to ensure the climate statements are in accordance with the Corporations Act (including the applicable AASB standards). This is a lower standard than the form of declaration that would ordinarily required.

This lower standard of declaration still leaves uncertainty as to precisely what steps will meet this "reasonable steps" standard.

Exactly when and what AUASB assurance requirements will be developed to assist directors in making the required declaration is also currently uncertain.

However, from the perspective of directors, this uncertainty is preferable to the position in the Exposure Draft, which had required a positive directors declaration in the ordinary form from the commencement of reporting, and before any assurance of climate statements had been expected to commence.

Mandatory climate-related disclosures will (subject to the limited exceptions below) be subject to the existing liability frameworks under the ASIC Act and Corporations Act in relation to director's duties, misleading and deceptive conduct provisions and general disclosure obligations.

However, the Bill contains a temporary "limited immunity" framework which applies for the first three years. It only applies to certain statements which are inherently uncertain. These "protected statements" are statements required to be made in a sustainability report (or in an auditor's report) and are limited to statements about:

scope 3 emissions;

scenario analysis; or

a transition plan.

During the first 12 months this limited immunity regime is also extended to a broader class of statements (contained in a sustainability report or auditors report) which "relate to climate" and are "about the future".

The limited immunity regime also applies to statements which are the same as "protected statements" (or are in the nature of updates or corrections to those statements) which are not contained in the sustainability report or auditors report themselves, but which are otherwise required to be made by a Commonwealth law (for example, under a continuous disclosure obligation or some other form of regulated disclosure document).

The effect of the limited immunity framework is to prevent claims in relation to "protected statements" unless the proceedings are either brought by ASIC or are criminal in nature. In other words, the regime is intended to exclude such claims by civil litigants (eg. securities class actions, or actions brought by third party litigants alleging greenwashing in respect of an entity's statements).

Those entities that will be covered by the new mandatory reporting framework should be taking steps now and seeking appropriate advice on governance, risk management, strategy, transition planning and scenario and climate resilience analysis, determining appropriate metrics and targets and collating information to report on their greenhouse gas emissions.