Geoff Hoffman

Chief Legal Officer •

Sydney

On 12 January 2024, the Government released the exposure draft Treasury Laws Amendment Bill 2024: Climate-related financial disclosure. The Exposure Draft contains amendments to the Australian Securities and Investment Commission Act 2001 (Cth) (ASIC Act) and the Corporations Act 2001 (Cth) which will require standardised, internationally-aligned climate-related financial reporting by companies and registered schemes and superannuation entities.

The Exposure Draft largely reflects the Government's proposals outlined in June 2023 in its second Consultation Paper, but with some important modifications.

Consultation for the Exposure Draft is very short. Submissions will close 9 February 2024.

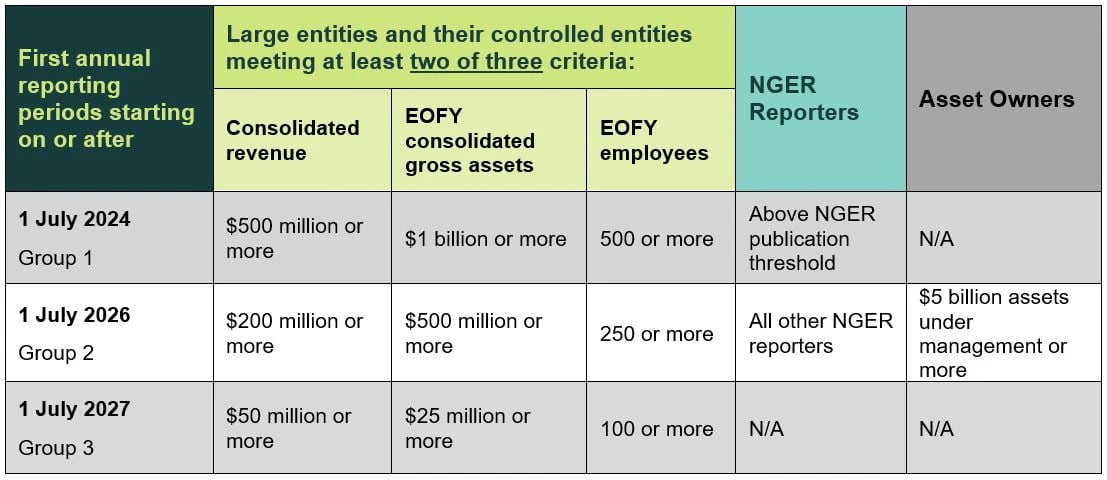

The Exposure Draft confirms that the new mandatory reporting requirements will apply to entities that are required to prepare and lodge annual reports under Chapter 2M of the Corporations Act. It also confirms the phased introduction outlined in the second Consultation Paper, with some significant changes.

An entity will now fall within Group 2 (below) if it is an asset owner (eg. a registered scheme or superannuation entity) where the value of its assets at the end of the financial year (including the entities it controls) is equal to or greater than $5 billion - even if it would not otherwise meet the other financial criteria. Similarly, entities with emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007 (Cth) (NGER Act) will fall within Group 2, regardless of size.

The table below summarises when entities must commence mandatory disclosure:

The Exposure Draft allows for the following exemptions.

Entities which fall within Group 3 and have no material climate-related risks or opportunities are only required to disclose a statement to that effect.

Entities that are registered under the Australian Charities and Not-for-profits Commission Act 2012 (Cth) are not required to prepare climate-related financial disclosures as part of their financial reporting obligations under that Act.

The Exposure Draft contains amendments to Part 2M.3 of the Corporations Act which require the entity to prepare a sustainability report containing climate statements which comply with the "sustainability standards" to be developed by the Australian Accounting Standards Board (AASB). This is in addition to the existing directors report, financial report, and auditors report included in the annual report .

As noted in the second Consultation Paper the sustainability standards will, broadly, include:

The AASB (which is currently developing Australian climate disclosure standards) decided not to publish the industry-based guidance accompanying IFRS S2, or include references to Sustainability Accounting Standards Board (SASB) Standards, until the content has been comprehensively internationalised by the International Sustainability Standards Board (ISSB) and has undergone the AASB’s own due process.

The AASB is proposing to introduce an Australian-specific requirement that if an entity elects to make industry-based disclosures, the entity should consider the applicability of well-established and understood metrics associated with the business models, activities or other common features that characterise participation in the same industry.

The Exposure Draft empowers the AASB to develop Australian climate disclosure standards, which the Government intends will closely align with ISSB’s IFRS S2 Climate-related Disclosures standards (IFRS S2).

On 23 October 2023, the AASB released Exposure Draft ED SR1 Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information to propose climate-related financial disclosure requirements. It is open for comment until 1 March 2024.

The Exposure Draft provides that an entity's sustainability report will only be subject to the audit and assurance requirements that apply to financial reports from 2030.

In the meantime, the Exposure Draft requires that an entity must have the statements in its sustainability report relating to scope 1 and 2 emissions reviewed by its auditor – and obtain a "review opinion" only (being a negative assurance that in the course of its review the auditor has not become aware of any non-compliance).

The specific extent and level of assurance required will be set out in the Australian assurance standards for climate disclosures to be developed by the Australian Auditing and Assurance Board (AUASB).

The directors of the entity will (as is the case with financial reports) still be required to provide a positive director's declaration that the sustainability report complies with the requirements of the Corporations Act (which includes compliance with the Sustainability Reporting Standards prepared by the AASB). This is the case notwithstanding:

Climate disclosures will (subject to the limited exceptions below) be subject to the existing liability frameworks under the ASIC Act and Corporations Act in relation to director's duties, misleading and deceptive conduct provisions and general disclosure obligations.

As foreshadowed in the second Consultation Paper, the Exposure Draft limits some of these liabilities by modifying the statutory liability regime for a limited period.

The limitations only apply to statements made in the Sustainability Report (and not if they are repeated outside the report) and only to two discrete parts of the sustainability report, being:

Further, the limitations only apply to statements made in sustainability reports prepared for financial years commencing between 1 July 2024 and 30 June 2027.

The limitations provide that only ASIC (and not other parties) will be able to bring proceedings for contraventions of the law relating to the above statements during the 3-year period referred to above.

The Exposure Draft also limits the kinds of actions that ASIC can bring to criminal prosecutions, and actions which are "civil in nature" which either:

While the proposed legislative drafting leaves some uncertainty – the broad effect of the provisions is to allow ASIC to bring proceedings under the civil penalty regime – but to limit its ability to seek pecuniary penalties to contraventions of legislative provisions that require the person to have been (at least) negligent in their conduct.

The Exposure Draft also includes a regime which enables ASIC to direct entities to correct statements in sustainability reports that are incorrect, incomplete, or misleading. This regime also only applies to sustainability reports prepared for financial years commencing between 1 July 2024 and 30 June 2027

Those entities that will be covered by the new mandatory reporting framework should be taking steps now and seeking appropriate advice on governance, strategy, transition planning and scenario and climate resilience analysis as well as collating information to report on their greenhouse gas emissions.