Stuart Byrne

Partner •

Sydney

Industry participants should consider whether to modify their research guidelines for capital markets transactions in the pipeline ahead of this transition date to minimise any potential reputational risk.

ASIC recently published its new Regulatory Guide 264: Sell-side research(RG 264) on sell-side analyst research. RG 264 is the result of an extensive review into the practices of sell-side research and corporate advisory and the potential conflicts of interest that may arise. Issuing companies, vendors, investment banks, research firms and financial advisers need to be across these lengthy guidelines to avoid tripping up with the regulator.

As with any ASIC policy guidance, an industry consultation process was conducted over the course of 2017. Coming out of this process, ASIC has relaxed some of the more troubling proposals in its Consultation Paper 290: Sell-side research (CP 290), such as the proposed prescriptive requirement for compliance to chaperone interactions.

Even so, there are some prescriptive guidelines being introduced regarding the interactions between research analysts and other parties to a capital raising process and investor education reports (IERs) which should be closely considered. Some of these guidelines are designed to reduce the risk of research analysts being unduly influenced by internally housed corporate advisory teams to provide a favourable view. As such, these guidelines may present opportunities for independent research providers or financial advisers.

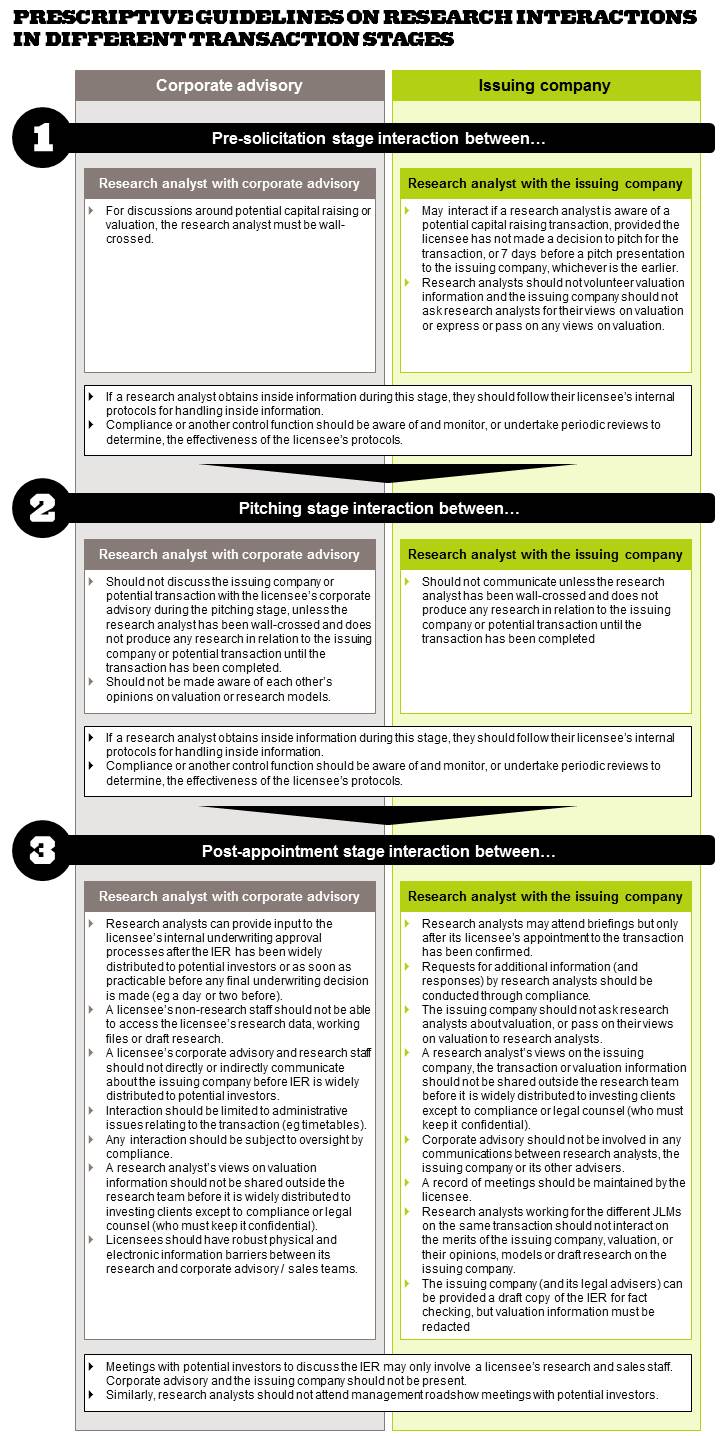

Key issue - prescriptive guidelines on research interactions in different transaction "stages"

In RG 264, ASIC has divided capital markets transactions into three stages, and below is a high-level summary of the new guidelines around the interactions between the parties involved at the different stages. A more detailed summary is at the bottom of this article.

Pre-solicitation (first becoming aware of a potential transaction and includes transaction vetting):

Research analysts may interact with corporate advisory and the issuing company provided that they have been wall-crossed. Without restricting discussions regarding valuation with corporate advisory, ASIC suggests that research analysts should not volunteer valuation information to the issuing company, and similarly, the issuing company should not ask research analysts about their views on valuation and not communicate to research analysts their own views.

Pitching (when a licensee decides to pitch, or 7 days before a pitching presentation, whichever is the earlier):

Research analysts may interact with corporate advisory and the issuing company provided that they have been wall-crossed and do not produce any research in relation to the issuer or transaction until the transaction has been completed. ASIC also suggests that corporate advisory and research should not share valuation information and research models during this pitching stage. It will be interesting to test whether this extends to discussion of valuation methodologies. Further, the bright line test for when the "pitching stage" occurs appears to encourage issuing companies to engage research analysts earlier rather than later. However, ASIC's guidance suggests that issuing companies should only brief analysts after the briefing of analysts should only happen after the licensee has been appointed

Post-appointment (when the licensee has been advised whether it has been selected to manage a deal):

A licensee's research analysts and corporate advisory should not communicate directly during this period about the issuing company before the IER is widely distributed (any interactions should be subject to direct oversight). It appears that this restriction is only limited to investment banks with internally housed corporate advisory and research functions. An exception is that research analysts can provide input and their views on the issuing company to the underwriting committee, but only immediately preceding any underwriting decision (eg. a day or two before). The other important guideline is that research analysts should not attend management roadshows with potential investors.

Key issue - guidelines on investor education reports

A number of key observations in relation to ASIC's guidance on IER related matters are outlined below:

Content: The IER may contain valuation information or assumptions provided they are based on the prospectus financials, including the forecasts disclosed in a prospectus. The drafting is unclear about whether research analyst assumptions in relation to DCFs and forecasts can be included. Valuation information should be expressed as an enterprise value or total value of the issuing company to reduce the risk of leaking inside information. ASIC is clear that the IER should not be used as a means to communicate company information, estimates or plans that are not in the prospectus.

Draft IERs: Draft IERs may only be released to compliance, the issuing company or its legal advisers to facilitate fact checking, with valuation information redacted. It is suggested that compliance should manage the distribution process for the draft redacted IER, including sending and receiving comments from the issuing company and its legal advisers. This might re-spark the debate about the desire for valuations to be included in research, which is not a universal practice around the world.

Fact-checking: Corporate advisory may not participate in the fact-checking of IERs before they are published. This puts more pressure on the fact checkers to get it right and an issuing company should ensure adequate time in typically tight timetables to do this. This may also mean additional costs if legal advisers are needed to assist with the fact checking.

Final IER: The final copy of the IER (unredacted, including valuation information) may only be provided to the issuing company after it has been widely distributed to potential investors. Any meetings with potential investors to discuss the IER should not involve corporate advisory, the issuing company or its other advisers.

Withdrawing / amending IER: ASIC has gone back on its original proposal in CP 290 prohibiting the withdrawal or amendment of the IER. IER may be withdrawn if errors are identified or new information becomes available which renders statements or information in the IER materially false, misleading or deceptive.

Other key issues to note

RG 264 contains guidance on a number of areas which we will briefly note:

Analyst declarations: ASIC has relaxed its proposed requirement (in CP 290) to require research analysts to provide a public declaration to compliance prior to the publication of research. ASIC no longer proposes that research analysts need to publicly disclose whether they have been in contact with the company subject to research, and no longer need to definitively declare whether they have insider information or that their research contains inside information. However, research analysts will need to provide a declaration to their compliance team that to the best of their knowledge, they are not in receipt of inside information and no other part of the firm has tried to influence the research.

Disclosure of interests: ASIC's proposed guidance in CP 290 required research reports to include prescriptive disclosures of interests including the number of shares and options (including the average price for shares and average exercise price for options) held by research analysts and the five largest share and option holders at the licensee. While this prescriptive requirement has now been relaxed, ASIC still requires prominent, specific and meaningful disclosure by the licensee of material interests (including beneficial interests) in the securities of the entity being covered by the research report.

Compliance function: ASIC has now toned down the language regarding its expectations of compliance functions but instead provide broader guidelines, for example, ASIC no longer indicates that compliance is required to attend analysts briefings / site visits in the post-appointment stage. However, ASIC's guidance suggests that compliance should be aware of and monitor, or undertake periodic reviews of, the interactions between research analysts, corporate advisory and issuing company and its other advisers. Research models and draft IERs should only be distributed through and managed by compliance.

Discretionary fees: ASIC has dropped its previous proposal in CP 290 to hide any discretionary fee arrangements from research analysts and having to redact the fees from copies of draft prospectuses which would be received by analysts. However, ASIC suggests that licensees should have robust controls to manage any conflicts of interest that may be derived from these fee arrangements.

Research coverage criteria: ASIC has softened its prescriptive proposal in CP 290 to require licensees to publish on their website their criteria and methodology for selecting a company for research coverage. The guidance now leaves it open to how a research provider can make it clear how they make coverage decisions.

Transitional period until 1 July 2018

ASIC has given the industry until 1 July 2018 to ensure that the compliance procedures of participants conform to its new guidelines. However, ASIC's new policy intends to demonstrate "best practice", and industry participants should consider whether to modify their research guidelines for capital markets transactions in the pipeline ahead of this transition date to minimise any potential reputational risk.

Detailed summary of the guidelines around research interaction in the different transaction stages.