Keshni Maharaj

Partner •

Sydney

When the Victorian Government handed down the 2019-20 Budget on 27 May 2019, we (along with other observers) thought we had a good handle on what revenue measures would be enacted. The State Taxation Acts Amendment Bill 2019, which was passed last night and is awaiting Royal Assent, [*] incorporates a number of significant stamp duty changes which were not announced as part of the Budget, including in respect of fixtures and the overhaul of the "economic entitlement" provisions. The changes to the economic entitlement provisions are sending shockwaves in the property industry, as no industry consultations were sought by the Victorian Government and also because these changes practically introduce a new head of duty in the Duties Act 2000 (Vic).

In this article we'll focus on the main changes brought in by the Bill, particularly those to the Duties Act and foreign resident surcharge for land tax (you can learn about the other main payroll tax and land tax measures from the 2019-20 Victorian Budget here).

Currently, certain intra-group transactions between 90% owned corporate groups involving Victorian "dutiable property" (including certain intra-group transactions involving Victorian "landholder" entities) are eligible for a 100% "corporate reconstruction exemption" (CRE) from Victorian duty. Any CRE granted under the current CRE regime is also subject to any conditions specified by the Victorian Commissioner and can be revoked by the Victorian Commissioner in certain circumstances such as if, subject to certain exceptions, the general three year post-association requirement is not satisfied (ie. the relevant members of the corporate group must remain members of that group for three years following the eligible CRE transaction taking place).

The key changes to the CRE regime under the Bill which will commence on 1 July 2019 (subject to transitional provisions referred to below) broadly include:

The Bill contains transitional provisions so that the existing CRE provisions (including the 100% exemption and the three year post association requirement) will continue to apply to:

The removal of the revocation provisions and the Commissioner's power to impose conditions means that eligible CRE transactions post 1 July 2019 will no longer be subject to any on-going conditions. However, the move to a 90% concessional model for CRE rather than a 100% exemption is a significant change that is out of step with other Australian State and Territories.

Key takeaway: Depending on the value of the "dutiable property" the subject of the corporate reconstruction application, a 10% impost for some intra-group transactions could be a significant cost and prevent genuine reconstruction transactions from being implemented.

The Victorian Duties Act currently contains provisions which are unique to Victoria and under which, Victorian landholder duty is charged on the acquisition by a person of certain entitlements in a private Victorian "landholder".

These entitlements include, amongst other things:

Although the Explanatory Memorandum to the Bill explains the amendments as being in response to the decision by the Victorian Supreme Court in BPG Caulfield Village Pty Ltd v Commissioner of State Revenue [2016] VSC 172 (BPG Caulfield Village), these amendments in fact go much further.

In BPG Caulfield Village, the Victorian Supreme Court held that the "economic entitlement" provisions could not be applied by the Commissioner where the relevant "economic entitlement" did not relate to all of the Victorian landholdings of the relevant private Victorian "landholder". This enabled taxpayers to arrange their affairs whereby the economic entitlements were only given in respect to a fraction of all the landholdings of the landholder.

Also under the current provisions, the "economic entitlement provisions" only applied to landholdings of private unit trusts and private companies. They do not currently apply to individuals, partnerships or discretionary trusts.

However, the amendments go much further than fixing the gap in the legislation. Firstly, post-amendments, the "economic entitlement" provisions will not be part of the "landholder duty" provisions, but will be a part of the transfer duty provisions. The Bill is effectively introducing an entirely new head of duty into the Duties Act.

The new "economic entitlement" transfer duty provisions can broadly be summarised as:

The Explanatory Memorandum states that the 100% deeming provision is an integrity measure which is intended to ensure that taxpayers do not understate "economic entitlements" by representing the benefit as fees, bonuses, charges and other amounts.

While the new "economic entitlement" provisions will take effect the day after the Bill receives Royal Assent, there are transitional provisions which provide that the new provisions do not apply to an arrangement made before the Bill receives Royal Assent.

The new "economic entitlement" provisions will be of particular concern to developers, agents or any person or entity who derives income or charges fees or any amounts calculated by reference to landholdings in Victoria. Intermediaries who facilitate the sale of large blocks of land to developers and are paid fees by reference to price paid for the land to the vendor by the developer may also find themselves on the wrong side of these provisions. Further, the deeming provisions imputing persons with having acquired 100% of the beneficial ownership of "relevant land" can be a trap for unsuspecting taxpayers who do not know about the introduction of these provisions and are continuing on with business as usual.

Key takeaway: Obtaining legal advice before undertaking any transactions which pertain to payments made by reference to Victorian land is imperative so that taxpayers are aware of their Victorian stamp duty liabilities and more importantly are not caught out by the 100% deeming provision.

Under the current Victorian Duties Act, "dutiable property" is defined to include amongst other things, certain specified estate or interests in land in Victoria. However, under the Bill an interest in certain fixtures (including tenants fixtures) will now also become "dutiable property" (Dutiable Fixtures).

Importantly, Dutiable Fixtures will not be subject to duty unless the unencumbered value of the Dutiable Fixtures exceeds $2,000,000. Further, there will be a phasing-in of duty under which concessional duty is payable on Dutiable Fixtures with an unencumbered value of $2,000,000 to $3,000,000, with full duty only payable where the unencumbered value exceeds $3,000,0000.

Interestingly, the Explanatory Memorandum to the Bill provides that the unencumbered value threshold of $2,000,000 relates to the Dutiable Fixtures taken as a whole and not the unencumbered value of the interest in the Dutiable Fixtures acquired by the transferee under the transaction. By way of example from the Explanatory Memorandum, if a transferee acquires a 50% interest in Dutiable Fixtures with an unencumbered value (as a whole) of $2,500,000, the exemption will not apply as the unencumbered value (as a whole) exceeds $2,000,000 even though the transferee is only acquiring an interest in Dutiable Fixtures with an unencumbered value of $1,250,000 (ie. $2,500,000 x 50%).

Additionally, under the Bill, aggregation will apply to separate dutiable transactions involving Dutiable Fixtures or a combination of Dutiable Fixtures and Victorian land if the dutiable transactions together form, evidence, give effect to, or arise from substantially one arrangement. Importantly the existing 12 month requirement under the current aggregation provisions (under which the relevant sale contracts in respect of the dutiable transactions must have been entered into within 12 months of each other or the dutiable transactions must occur within 12 months of each other) do not apply in circumstances where one of the relevant "dutiable transactions" relates to Dutiable Fixtures.

While these new provisions in respect of Dutiable Fixtures will take effect the day after the Bill receives Royal Assent, there are transitional provisions which provide that the new provisions do not apply to an arrangement made before that time.

Under the Bill, the foreign resident surcharge in Victoria (which is in addition to the general stamp duty/land tax rate) for:

Effectively this will increase the maximum rate of stamp duty payable by foreign residents on transactions involving residential property as 13.5%. Importantly, the foreign resident surcharge is not solely applicable to Victorian land which contains residential premises. For example it is also applicable to foreign residents who acquire Victorian land on which they intend to construct residential premises. Further the foreign resident surcharge for land tax is not restricted to residential property and applies to Victorian land owned by foreign residents irrespective of the property type.

Under the Bill a 10% stamp duty concession will be introduced from 1 July 2019 in respect of the "eligible transfers" of Victorian land or Dutiable Fixtures which are wholly located in regional Victoria and the transferee intends to use the Victorian land or Dutiable Fixtures for a "qualifying use".

A "qualifying use" is a land use described in the Australian Valuation Property Classification Code, based on the Valuation Best Practice Specification Guidelines in the ranges 210 to 299 or 310 to 499.

The concession will originally commence for contracts / arrangements / agreements entered into on or after 1 July 2019 at a 10% rate, and will incrementally increase by 10% from 1 July 2020 to 50% by 1 July 2023.

The Victorian Duties Act will be amended to remove a restriction that prevents a "unit trust scheme" that was at any time eligible for registration as a "wholesale unit trust scheme" from being a "public unit trust scheme".

This means that a wholesale unit trust scheme can now be converted into a listed unit trust or a widely held unit trust, but only upon payment of 10% of the landholder duty that is currently payable for converting private unit trust schemes into public unit trust schemes in Victoria.

The acquisition threshold for landholder duty to apply in Victoria is 50% and for public unit trust schemes it is 90%.

The amendments in relation to wholesale unit trusts schemes will apply from the day after the Bill receives Royal Assent.

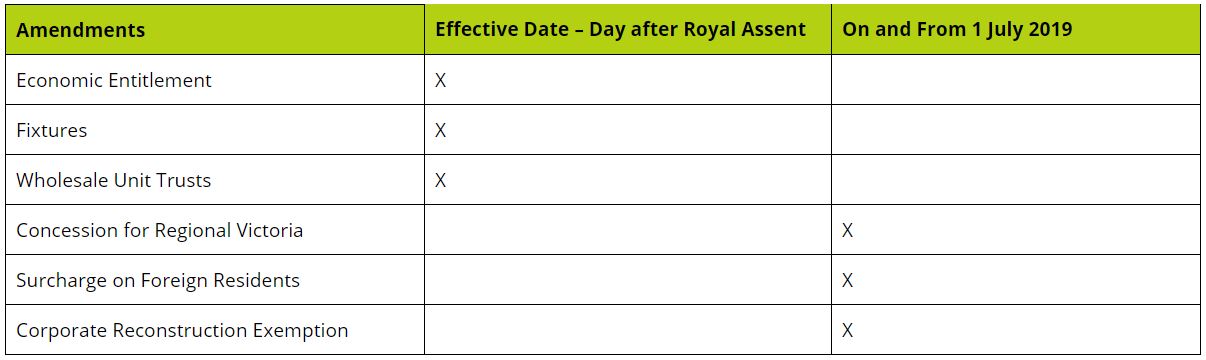

Be aware of the key dates

[*] Royal Assent was given on 18 June 2019 Back to article