Keshni Maharaj

Partner •

Sydney

Since their inception, the "sub-sale" provisions in the Victorian stamp duty legislation have become a "double duty" trap for unwary developers, purchasers and investors. In a well-intentioned move, the State Revenue Office of Victoria has issued guidelines in the form of Ruling DA-064 on the meaning of "land development" in the context of the specific "sub-sale" provisions. Developers, purchasers and investors should now be getting new stamp duty advice which reflects this.

The "sub-sale" provisions are contained in Part 4A of Chapter 2 of the Duties Act 2000 (Vic).

In very broad terms, in the context of "land development", the "sub-sale" provisions in the Victorian stamp duty legislation can apply if:

While the "sub-sale" provisions can also be enlivened where there is the provision of certain "additional consideration", this is not covered as part of this article given it relates to separate provisions under the "sub-sale" provisions.

Part of the issue is driven by the inherent complexity of the "sub-sale" provisions and the broad definition of "land development" for the purposes of the "sub-sale" provisions which extends beyond the ordinary meaning of the term (to include, for example, preparing a plan of subdivision or applying for certain permits or approval etc.).

For illustrative purposes, this is one of the more common scenarios where the "sub-sale" provisions can be enlivened in the context of "land development":

Consequently, subject to certain limited exceptions, if "land development" takes place between the contract date and the date the land is transferred to the Subsequent Purchaser, then two lots of duty can potentially be charged – firstly on the sale contract (ie. as if it had been completed by the First Purchaser) and secondly on the Subsequent Transaction. There can also be other lots of duty depending on if there are multiple nominations and / or "Subsequent Purchasers" etc. For illustrative purposes, one of the limited exceptions (and also one of the most important) is if the "land development" occurred after the "Subsequent Purchaser" obtained a "Transfer Right".

For the purposes of the "sub-sale" provisions, "land development" has a very broad definition which extends beyond what is generally considered land development under its ordinary meaning. This is one of the key reasons that the "sub-sale" provisions have been a 'double duty' trap since their inception.

While the ordinary meaning of "land development" might suggest an activity involving a change to the physical condition of the land (such as physically pouring concrete on the ground etc.), for the purposes of the "sub-sale" provisions, "land development" can comprise activities which do not involve, or take place prior to, any physical development activities being commenced on the land.

It will comprise any one or more the following six Limbs:

Importantly, under the Guidelines Limbs 1 to 5 can comprise "land development" regardless of whether the corresponding activities undertaken actually lead to an increase in value or change in utility of the land.

In determining whether an activity constitutes "land development" under the six limbs, the Commissioner will consider:

Further, the Commissioner's scrutiny of activities that are directly or indirectly undertaken will not be limited only to the conduct of the parties to any sale contract / agreement / nomination. It will also extend to relevant activities directly or indirectly undertaken by related parties, agents, associates and tenants of the parties. This is an important point because it emphasises the responsibility that is placed on certain transaction parties (ie. First Purchasers and Subsequent Purchasers) for the purposes of any potential enlivenment of the "sub-sale" provisions to ensure that they are aware of all activities which are proposed to be undertaken, or which are being undertaken, in respect of the land, even if such activities are not being undertaken by them.

The Guidelines provide commentary (and examples) for each Limb, but we will focus on Limbs 1 and 6 below as they have caused particular confusion.

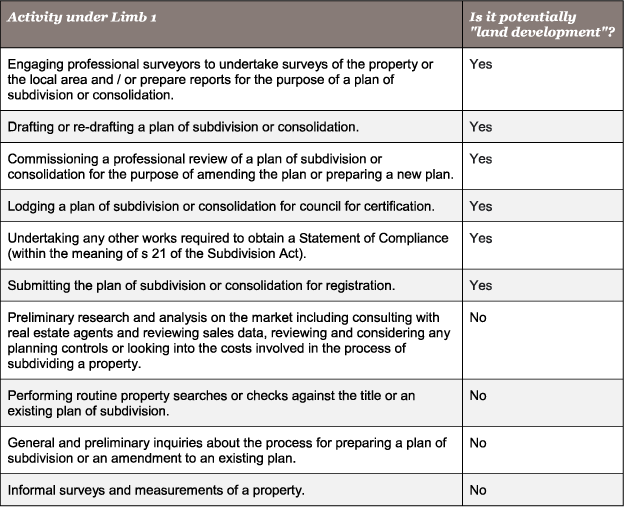

Undertaking subdivision, consolidation and other plan registration activities are often key aspects of any development of land.

In broad terms, the table below sets out the activities described in the Guidelines and which the Commissioner considers potentially falls or does not fall within the scope of Limb 1.

Importantly, the Commissioner's view is that initial activities undertaken to prepare a plan or measures taken to have a plan registered can constitute "land development". However, in practice, it may be difficult to determine whether an activity or a measure is merely "preliminary" (and therefore not "land development") or whether it constitutes "land development" for the purposes of Limb 1. Accordingly, we recommend that care be taken when engaging or instructing surveyors and internal and external consultants (including when defining the scope of the engagement and instructions).

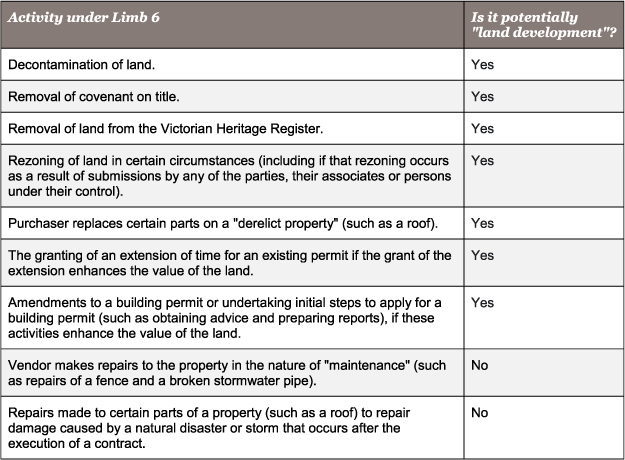

Limb 6 – Developing / changing land in any other way that would lead to enhancement of its value

Based on the Guidelines, the Commissioner considers that Limb 6 is a quasi catch-all limb for all activities outside of Limbs 1 to 5 if those activities enhance the value of the land.

Practically therefore, the precise scope of Limb 6 is very broad and uncertain, and it is important for entities (ie. First Purchasers and Subsequent Purchasers) to be mindful that even if a specific activity does not fall within Limbs 1 to 5, it could still be determined by the Commissioner to fall into Limb 6 if considered to enhance the value of the land. For example, it is not clear, based on the Guidelines, if any leasing activities (such as entering into an agreement for lease with a tenant) could fall within the scope of Limb 6.

In broad terms, the table below sets out the activities described in the Guidelines and which the Commissioner considers potentially falls or does not fall within the scope of Limb 6.

Furthermore we note the following from the Guidelines:

The Guidelines are not binding on the Commissioner and are not exhaustive. Instead, they demonstrate the Commissioner's approach when determining whether "land development" has occurred for relevant purposes, and they illustrate the broad discretionary powers that the Commissioner has in this regard.

Although in some respects the Guidelines provide much needed clarification, there is still uncertainty for the parties. Given these matters and the complexity of the sub-sale provisions, it is possible that:

Land developers, purchasers and investors will need to familiarise themselves with the Guidelines and ensure that they engage in a robust process of considering the following questions (ideally before entering into a sale contract or option):

Given the complexity of the "sub-sale" provisions and the potentially significant consequences of falling into the "double duty" trap, land developers, purchasers and investors should seek specialised stamp duty advice, particularly before entering into a sale contract or option and prior to undertaking any activity which could potentially comprise "land development" or could otherwise trigger any enlivening of the "sub-sale" provisions.